Repo market basics

An overview of repo market mechanics and its relationship with financial markets

A close friend who works at a repo desk here in Canada suggested I read “Canadian Repo Market Ecology” by the BoC. I suspect this may have been because he is sick of answering my questions about what exactly he does…

Regardless, here are the basics I learned about the repo market.

Introduction

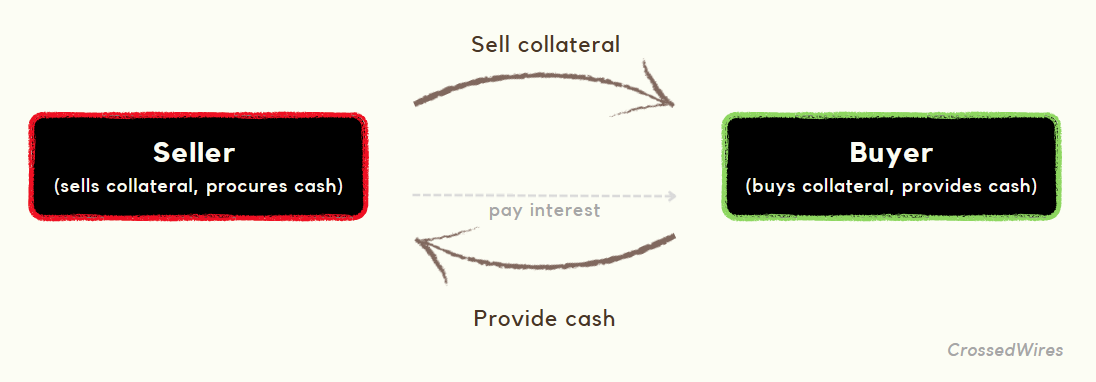

A repurchase agreement, or repo, is a collateralized loan agreement between two parties. The seller gives up an asset (collateral) in return for immediate cash, and the buyer provides cash to the seller at a predetermined interest rate.

Repos are special for several reasons:

They provide short term leverage (days to months) for institutional investors

They come with a repurchase date when the collateral will be bought back

Any income from the posted collateral is paid back to the seller (an added incentive to borrow with collateral)

The collateral is owned by the buyer for the duration of the repurchase agreement

Since collateral ownership changes, the new owner can reuse the collateral in another repo agreement

A reverse repo is simply a repo seen from the perspective of the buyer. So when you see a headline like:

“103 COUNTERPARTIES TAKE $2.199 TLN AT THE FED REVERSE REPO OPERATION”

This means that the fed has taken ownership of $2.199T of assets and given out a bunch of cash (for a posted interest rate).

Participants and Incentives

This market is primarily for institutional investors. It allows them to post assets such as GoC bonds or other securities (e.g. equity) as collateral from which they can (hopefully) produce additional income. The inverse of this allows the participant to borrow a desired security which is particularly useful when short selling.

The quality of the asset, as well as the credit rating of the seller institution impacts the interest rate they are charged for the repo.

In Canada, the largest players in the repo market are the usual suspects:

The big 6 banks (e.g., BMO, CIBC, RBC, etc.)

Major pension funds (e.g., CPP, OTPP, HOOP, etc.)

Other dealers / smaller banks (e.g., Desjardins, Equitable, etc.)

Banks in Canada generally hold lending positions on repos, faciliting borrowing needs for their clients.

Base cases for using repos:

Enhance yields / increase leverage for reinvestment

Repo an existing asset, gain 2x cash, reinvest in a higher yield product

Short bonds

Sell a bond on the open market and borrow it in repo to cover delivery

Manage balance sheet asset mix

Since a bond purchase via reverse repo is an explicit change in ownership, financial institutions can undertake a repo to meet compliance requirements

Carry trades

If no changes in yield curve is expected, a desk can utilize a repo to provide short term financing for re-investment in a longer term bond and earn the spread between the bond yield and repo rate

Relationship with equity markets

Everything is interrelated in financial markets. The repo market consists of large institutional inverstors borrowing or lending collateral for short term leverage.

In the US market, Secured Overnight Financing Rate (SOFR) is a typical measure of borrowing cash overnight, collateralized by treasury securities (i.e., a repo)

Lets have a look at the relationships between SOFR and:

The fed funds rate

30y, 10y, 5y, and 2y treasury yields, and

SPX index

First, Fed funds (purple) vs. SOFR (red): we see a clear correlation here as expected…

Next, lets add in US Treasury yields: correlated but with UST yields rising at a much faster pace (2y has been the big story)

Finally, lets add SPX (green) to the mix: inverse correlation between SOFR and SPX (particularly noticeable post covid with SOFR close to 0 for ~2 years)

This seems to reinforce the narrative that cheap debt can fuel equity growth.

Summary

At a very high level, repos enable liquidity in financial markets

They provide access to low cost, short term funding for institutions

Higher repo rates (e.g. CORRA, SOFR) would theoretically reduce incentive to borrow funds

Equity markets can have a tail / head wind from low / high repo rates (SOFR, CORRA)

Well that’s it for the basic stuff. Rest assured, there are a lot more intricacies about repo markets not covered here. If you would like to know more, you can find links to the source material below.

Sources & Further reading

The paper from BoC can be found here: https://www.bankofcanada.ca/2016/03/staff-discussion-paper-2016-8/

Dynamics of US overnight triparty repo: https://www.federalreserve.gov/econres/notes/feds-notes/the-dynamics-of-the-us-overnight-triparty-repo-market-20210802.html

Canadian overnight repo rate data: https://www.bankofcanada.ca/rates/interest-rates/corra/

Secured overnight financing rate data: https://www.newyorkfed.org/markets/reference-rates/sofr

Thanks for reading, please consider subscribing if you enjoyed this post!